Tutorial

tutorial.RmdThis page demonstrates the usage of the hbal package, which implements hierarchically regularized entropy balancing introduced by Xu and Yang (2022). hbal automatically expands the covariate space to include higher order terms and uses cross-validation to select variable penalties for the balancing conditions, and then seeks approximate balance on the expanded covariate space.

hbal provides two main functions:

hbal(): performs hierarchically regularized entropy balancing.att(): calculates the average treatment effect on the treated (ATT) from anhbalobject returned byhbal().

And two S3 methods:

summary(): summarizes the balancing results.plot(): visualizes covariate balance before and after weighting or the distribution of balancing weights.

R code used in this tutorial can be downloaded from here.

Basic Usage

We simulate a toy cross-sectional dataset with a binary treatment to illustrate the basic usage of hbal. Note that treatment assignment depends on all three covariates.

library(hbal)

set.seed(1984)

N <- 1500

X1 <- rnorm(N)

X2 <- rnorm(N)

X3 <- rbinom(N, size = 1, prob = .5)

D_star <- 0.5 * X1 + 0.3 * X2 + 0.2 * X1 * X2 - 0.5 * X1 * X3 - 1

D <- ifelse(D_star > rnorm(N), 1, 0) # Treatment indicator

y <- 0.5 * D + X1 + X2 + X2 * X3 + rnorm(N) # Outcome

dat <- data.frame(D = D, X1 = X1, X2 = X2, X3 = X3, Y = y)

head(dat)

#> D X1 X2 X3 Y

#> 1 0 0.4092032 1.37178450 0 0.6358481

#> 2 1 -0.3230250 0.62887225 0 1.5377304

#> 3 0 0.6358523 1.49692496 1 1.5998765

#> 4 0 -1.8461288 0.19218026 1 -1.8232558

#> 5 0 0.9536474 0.16077270 0 3.2611010

#> 6 0 1.1884898 -0.07989461 1 1.0611114hbal is an extension of entropy balancing, or

ebal proposed by Hainmueller

(2012). By default, hbal replicates

ebal by performing exact balancing on all covariates

and no serial expansion, i.e., expand.degree = 1 (default).

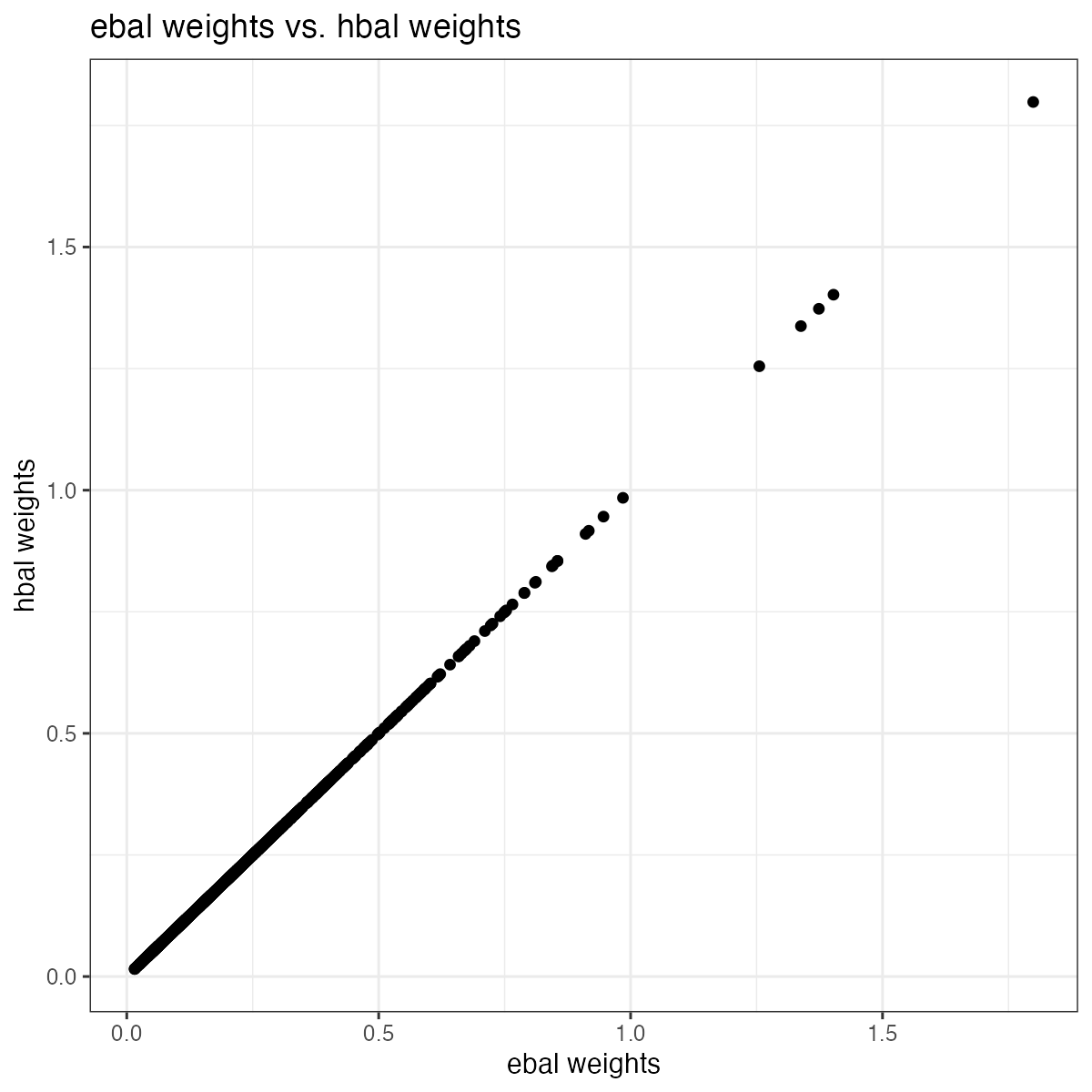

We can demonstrate this equivalence by showing the hbal weights are

exactly the same to the ebal weights from the ebal

package in this case.

library(ebal)

ebal.out <- ebalance(Treat = dat$D, X = dat[,c('X1', 'X2', 'X3')]) # ebal

#> Converged within tolerance

hbal.out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y', data = dat) # hbal

# plot weights

W <- data.frame(x = ebal.out$w, y = hbal.out$weights.co)

ggplot(aes(x = x, y = y), data = W) + geom_point() + theme_bw() +

labs(x = "ebal weights", y="hbal weights", title = "ebal weights vs. hbal weights")

hbal() returns a list of 15 objects:

names(hbal.out)

#> [1] "converged" "weights" "weights.co" "coefs"

#> [5] "Treatment" "mat" "grouping" "group.penalty"

#> [9] "term.penalty" "bal.tab" "base.weights" "Treat"

#> [13] "Outcome" "Y" "call"- converged: Binary indicator of whether the algorithm has converged.

- weights: Resulting weights, including the base weights for the treated and solution weights for the controls (see below).

- weights.co: Solution weights for the controls. Can be plugged into any downstream estimator.

-

coefs: Values of Lagrangian multipliers. They are

used to calculate the solution

weights. - Treatment: The treatment status vector.

- mat: Data matrix, including the outcome variable (the first column), the treatment variable (the second column), and expanded covariates (the remaining columns).

- grouping: A vector of the number of variables in each covariate group. The length of the vector equals the number of groups.

- group.penalty: Penalties for different groups of covariates. This is the regularization parameter \(\alpha\) in Xu and Yang (2022).

- term.penalty: Penalties for individual covariates. The length of the vector equals the number of balancing terms, including expanded ones.

- bal.tal: A balance table.

-

base.weights: A vector of base weights, originally

from variable

wsupplied by users. The length of the vector equals the number of rows entering the balancing scheme. - Treat: A character string that stores the treatment variable name.

-

Outcome: The outcome vector, if

Yis supplied. -

Y: A character string that stores the outcome

variable name, if

Yis supplied.. - call: A string of the function call.

The summary() function provides additional information

on the balancing scheme, including the numbers of treated and control

units, groups and corresponding penalties, and a balance table, in which

Std.Diff.(O) and Std.Diff.(W) represent

standardized difference before and after balancing, respectively. For

example, in this case, only the linear terms are being balanced on.

summary(hbal.out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y")

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0

#> X2 0.42 -0.07 0.42 0.49 0

#> X3 0.52 0.51 0.52 0.02 0In addition to balancing on just the linear/level terms of the

covariates, hbal() allows balancing on a serial expansion

of the covariates. This is achieved by setting the

expand.degree argument. Currently, hbal()

supports both second order serial expansion (two-way interactions and

square terms; expand.degree = 2) and third order serial

expansion (two-way interactions, square terms, linear*square

interactions, and cubic terms; expand.degree = 3). For

example, we can do exact balancing on third order serial expansion of

the covariates:

out <- hbal(Y = 'Y', Treat = 'D', X = c('X1', 'X2', 'X3'),

data = dat, expand.degree = 3)

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> expand.degree = 3)

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0

#> two-way 3 0

#> squared 2 0

#> three-way 1 0

#> squared*linear 4 0

#> cubic 2 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0

#> X2 0.42 -0.07 0.42 0.49 0

#> X3 0.52 0.51 0.52 0.02 0

#> X1.X2 0.24 -0.10 0.24 0.32 0

#> X1.X3 0.07 -0.02 0.07 0.12 0

#> X2.X3 0.21 -0.01 0.21 0.33 0

#> X1.X1 1.01 1.01 1.01 0.00 0

#> X2.X2 0.99 0.99 0.99 0.00 0

#> X1.X2.X3 0.13 0.00 0.13 0.18 0

#> X1.X1.X2 0.32 -0.01 0.32 0.18 0

#> X1.X2.X2 0.32 -0.17 0.32 0.29 0

#> X1.X1.X3 0.55 0.52 0.55 0.03 0

#> X2.X2.X3 0.50 0.47 0.50 0.02 0

#> X1.X1.X1 0.93 -0.25 0.93 0.30 0

#> X2.X2.X2 1.16 -0.23 1.16 0.40 0Obtaining the ATT

We can use att() on a hbal object to

directly get an ATT estimate. Note that att() uses linear

regression with robust standard errors (lm_robust() from

the estimatr package) to calculate the ATT.

att() allows users to use one of the following three

methods to estimate the ATT:

difference in weighted means by setting

dr = FASLE, in whichdrrepresents doubly robust; as a result,methodis ignored;weighted linear regression by setting

method = ""lm_robust"(default);weighted linear regression with a full set of interactions between the treatment indicator and demeaned covariates, or Lin’s method, by setting

method = ""lm_lin".

By default, att() only displays treatment

effect(displayAll = FALSE). Additional arguments accepted

by lm_robust() or lm_lin(), such as

se_type and clusters, can be passed to

att(), for example:

att(out, dr = FALSE)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> D 0.4762995 0.1598373 2.979902 0.002929846 0.1627709 0.7898281 1498

att(out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> D 0.4760107 0.0723624 6.57815 6.585301e-11 0.3340672 0.6179543 1483

att(out, method = "lm_lin", se_type = "stata")

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> D 0.4760117 0.07174978 6.634329 4.571141e-11 0.3352686 0.6167547 1468Setting displayAll = TRUE reveals the coefficients of

the intercept and covariates.

att(out, displayAll = TRUE)

#> Estimate Std. Error t value Pr(>|t|) CI Lower

#> (Intercept) -0.017925289 0.08071202 -0.2220895 8.242748e-01 -0.17624715

#> D 0.476010719 0.07236240 6.5781503 6.585301e-11 0.33406718

#> X1.1 1.076177748 0.08570502 12.5567645 1.926101e-34 0.90806179

#> X2.2 0.980125850 0.08413119 11.6499706 4.481064e-30 0.81509707

#> X3.3 0.089263107 0.10341474 0.8631566 3.881910e-01 -0.11359161

#> X1.X2.4 0.034941778 0.07166458 0.4875739 6.259238e-01 -0.10563295

#> X1.X3.5 0.022640656 0.09878060 0.2292014 8.187440e-01 -0.17112391

#> X2.X3.6 0.977725257 0.09160442 10.6733410 1.128674e-25 0.79803723

#> X1.X1.7 0.031742608 0.06485248 0.4894586 6.245894e-01 -0.09546974

#> X2.X2.8 -0.027041722 0.05013758 -0.5393503 5.897261e-01 -0.12538985

#> X1.X2.X3.9 0.005037062 0.08429199 0.0597573 9.523570e-01 -0.16030716

#> X1.X1.X2.10 0.021959776 0.02717454 0.8081011 4.191620e-01 -0.03134485

#> X1.X2.X2.11 -0.028702480 0.03235373 -0.8871459 3.751442e-01 -0.09216642

#> X1.X1.X3.12 -0.072661510 0.07055546 -1.0298496 3.032486e-01 -0.21106063

#> X2.X2.X3.13 0.040315487 0.06078776 0.6632172 5.072945e-01 -0.07892365

#> X1.X1.X1.14 -0.014453206 0.01519561 -0.9511436 3.416864e-01 -0.04426038

#> X2.X2.X2.15 0.015701662 0.02432758 0.6454263 5.187508e-01 -0.03201847

#> CI Upper DF

#> (Intercept) 0.14039657 1483

#> D 0.61795426 1483

#> X1.1 1.24429371 1483

#> X2.2 1.14515463 1483

#> X3.3 0.29211782 1483

#> X1.X2.4 0.17551650 1483

#> X1.X3.5 0.21640522 1483

#> X2.X3.6 1.15741328 1483

#> X1.X1.7 0.15895496 1483

#> X2.X2.8 0.07130640 1483

#> X1.X2.X3.9 0.17038128 1483

#> X1.X1.X2.10 0.07526440 1483

#> X1.X2.X2.11 0.03476146 1483

#> X1.X1.X3.12 0.06573760 1483

#> X2.X2.X3.13 0.15955462 1483

#> X1.X1.X1.14 0.01535397 1483

#> X2.X2.X2.15 0.06342180 1483Furthermore, hbal() allows variable penalties on the

balancing conditions for different groups of covariates. Penalties are

automatically determined using cross-validation. This minimizes the

variance of the weights, increases the feasibility of the balancing

problem, and is the approach advocated in Xu and

Yang (2022). We can do so by setting cv = TRUE. Note

that, by default, hbal() only penalizes higher-order terms

and seeks to achieve exact balance on linear terms.

out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y',

data = dat, expand.degree = 3, cv = TRUE)

#> Crossvalidation...

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> expand.degree = 3, cv = TRUE)

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0.0

#> two-way 3 2.0

#> squared 2 0.0

#> three-way 1 21.2

#> squared*linear 4 6.3

#> cubic 2 0.0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0.00

#> X2 0.42 -0.07 0.41 0.49 0.00

#> X3 0.52 0.51 0.52 0.02 0.00

#> X1.X2 0.24 -0.10 0.08 0.32 0.15

#> X1.X3 0.07 -0.02 0.23 0.12 -0.22

#> X2.X3 0.21 -0.01 0.24 0.33 -0.04

#> X1.X1 1.01 1.01 1.01 0.00 0.00

#> X2.X2 0.99 0.99 0.99 0.00 0.00

#> X1.X2.X3 0.13 0.00 0.12 0.18 0.00

#> X1.X1.X2 0.32 -0.01 0.45 0.18 -0.07

#> X1.X2.X2 0.32 -0.17 0.24 0.29 0.05

#> X1.X1.X3 0.55 0.52 0.56 0.03 -0.01

#> X2.X2.X3 0.50 0.47 0.51 0.02 -0.01

#> X1.X1.X1 0.93 -0.25 0.93 0.30 0.00

#> X2.X2.X2 1.16 -0.23 1.16 0.40 0.00

att(out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> D 0.4829908 0.07347752 6.573313 6.796656e-11 0.3388598 0.6271217 1483Visualizing Results

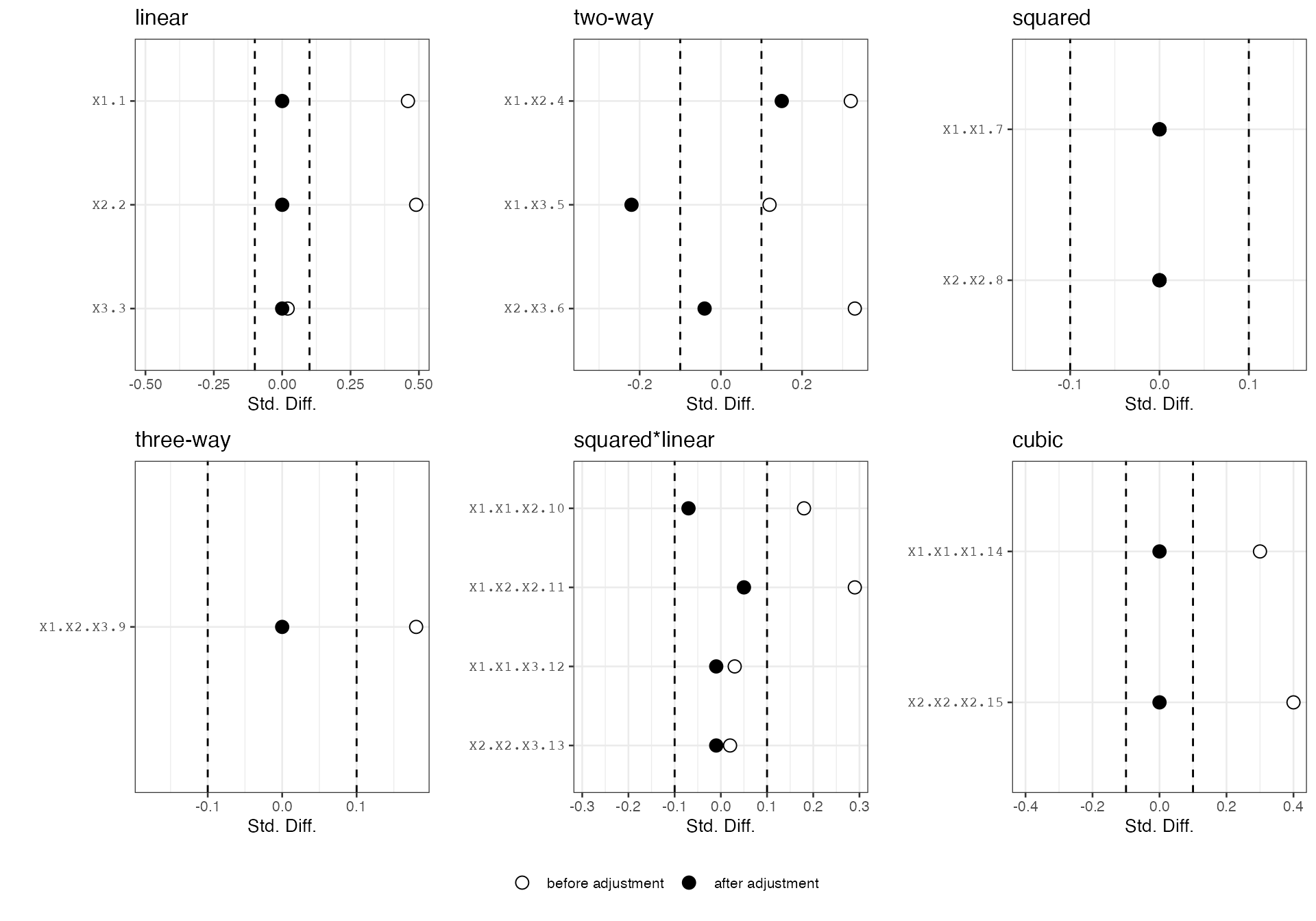

hbal has a build-in plot() method that

allows us to visualize covariate balance before and after balancing.

plot(out)

From the above plots, we can see that the linear terms of the covariates are exactly balanced between the treatment and the control groups. We can check the group penalties or penalties applied to each covariate. In this case, the higher-order terms all have relatively high penalties except for two-way interactions, in accordance with the true data generating process.

round(out$group.penalty, 2)

#> linear two-way squared three-way squared*linear

#> 0.00 1.98 0.00 21.21 6.34

#> cubic

#> 0.00

round(out$term.penalty, 2)

#> X1.1 X2.2 X3.3 X1.X2.4 X1.X3.5 X2.X3.6

#> 0.00 0.00 0.00 1.98 1.98 1.98

#> X1.X1.7 X2.X2.8 X1.X2.X3.9 X1.X1.X2.10 X1.X2.X2.11 X1.X1.X3.12

#> 0.00 0.00 21.21 6.34 6.34 6.34

#> X2.X2.X3.13 X1.X1.X1.14 X2.X2.X2.15

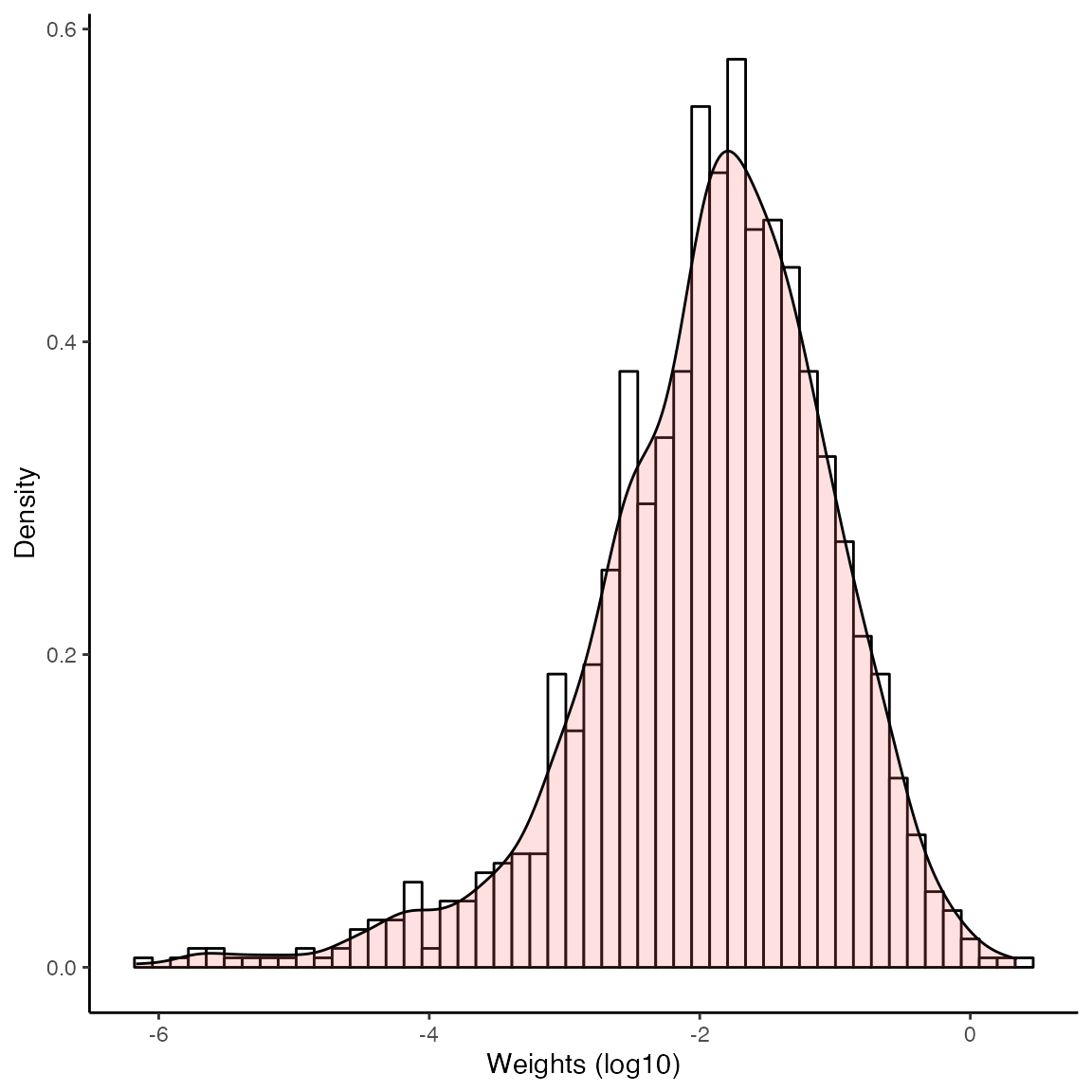

#> 6.34 0.00 0.00We can also plot the weight distribution for the control units by

specifying type = 'weight' in plot(). We can

see that the weights are quite concentrated around the unit weight.

plot(out, type='weight')

#> sum(weights) normalized to the number of treated units

Additional Options

Controlling Exact/Approximate Balancing

Users can manually control which group of covariates to be exactly

balanced and which group to be approximately balanced (via

regularization) by using the group.exact argument. It takes

in a binary vector with length equal to the number of covariate groups,

with 1 indicating exact balance on that group and 0 indicating

approximate balance. Appropriate penalties are then searched through

cross-validation. When using this option, please make that the length of

vector supplied equals the number of groups.

For example, we can ask hbal() to achieve exact balance

on the linear terms and two-way interactions and approximate balance for

the rest:

out <- hbal(Treat = 'D', X = c('X1', 'X2'), Y = 'Y', data = dat,

expand.degree = 3, cv = TRUE, group.exact = c(1, 1, 0, 0, 0))

#> Crossvalidation...

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2"), Y = "Y", expand.degree = 3,

#> cv = TRUE, group.exact = c(1, 1, 0, 0, 0))

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 2 0.0

#> two-way 1 0.0

#> squared 2 0.0

#> squared*linear 2 0.1

#> cubic 2 98.8

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0.00

#> X2 0.42 -0.07 0.42 0.49 0.00

#> X1.X2 0.24 -0.10 0.24 0.32 0.00

#> X1.X1 1.01 1.01 1.01 0.00 0.00

#> X2.X2 0.99 0.99 0.99 0.00 0.00

#> X1.X1.X2 0.32 -0.01 0.38 0.18 -0.03

#> X1.X2.X2 0.32 -0.17 0.34 0.29 -0.01

#> X1.X1.X1 0.93 -0.25 1.04 0.30 -0.03

#> X2.X2.X2 1.16 -0.23 0.96 0.40 0.06User-Supplied Penalties

If researchers have prior knowledge about covariates and would like

to supply specific penalties for each group of covariates, we can do so

by passing a vector of penalties to the group.alpha

argument. For example, we can manually set penalties to be 0 for the the

linear terms and two-way interactions and 100 for other groups:

out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y', data = dat,

expand.degree = 3, group.alpha = c(0, 0, 100, 100, 100, 100))

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> expand.degree = 3, group.alpha = c(0, 0, 100, 100, 100, 100))

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0

#> two-way 3 0

#> squared 2 100

#> three-way 1 100

#> squared*linear 4 100

#> cubic 2 100

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0.00

#> X2 0.42 -0.07 0.42 0.49 0.00

#> X3 0.52 0.51 0.52 0.02 0.00

#> X1.X2 0.24 -0.10 0.24 0.32 0.00

#> X1.X3 0.07 -0.02 0.07 0.12 0.00

#> X2.X3 0.21 -0.01 0.21 0.33 0.00

#> X1.X1 1.01 1.01 1.18 0.00 -0.12

#> X2.X2 0.99 0.99 1.06 0.00 -0.06

#> X1.X2.X3 0.13 0.00 0.14 0.18 -0.02

#> X1.X1.X2 0.32 -0.01 0.52 0.18 -0.11

#> X1.X2.X2 0.32 -0.17 0.37 0.29 -0.03

#> X1.X1.X3 0.55 0.52 0.58 0.03 -0.03

#> X2.X2.X3 0.50 0.47 0.55 0.02 -0.06

#> X1.X1.X1 0.93 -0.25 1.06 0.30 -0.03

#> X2.X2.X2 1.16 -0.23 1.03 0.40 0.04Controlling Serial Expansion

Sometimes we may not want to perform serial expansion on all

covariates but instead expand on a select set of covariates, we can do

so by using the X.expand argument to specify the covariates

we want to expand on. For example, we can expand only on

X1:

out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y', data = dat,

expand.degree = 3, X.expand = c('X1', 'X2'))

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> X.expand = c("X1", "X2"), expand.degree = 3)

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0

#> two-way 1 0

#> squared 2 0

#> squared*linear 2 0

#> cubic 2 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0

#> X2 0.42 -0.07 0.42 0.49 0

#> X3 0.52 0.51 0.52 0.02 0

#> X1.X2 0.24 -0.10 0.24 0.32 0

#> X1.X1 1.01 1.01 1.01 0.00 0

#> X2.X2 0.99 0.99 0.99 0.00 0

#> X1.X1.X2 0.32 -0.01 0.32 0.18 0

#> X1.X2.X2 0.32 -0.17 0.32 0.29 0

#> X1.X1.X1 0.93 -0.25 0.93 0.30 0

#> X2.X2.X2 1.16 -0.23 1.16 0.40 0Selecting Covariates

Performing serial expansion on many covariates can result in a

prohibitive number of covariates that need to be balanced on. In such

cases, users many want to reduce the number of covariates by using the

double selection method by Belloni, Chernozhukov,

and Hansen (2014). This screens the expanded covariates and only

keeps those that are predictive for the treatment assignment or the

outcome. Users can enable double selection by setting

ds = TRUE. In the following case, almost all the

higher-order terms except X1*X2 and X2*X3 are

screened out by the double selection procedure.

out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y', data = dat,

expand.degree = 3, ds = TRUE)

summary(out)

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> expand.degree = 3, ds = TRUE)

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 2 0

#> two-way 2 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0

#> X2 0.42 -0.07 0.41 0.49 0

#> X1.X2 0.24 -0.10 0.24 0.32 0

#> X2.X3 0.21 -0.01 0.21 0.33 0

att(out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> D 0.4789838 0.07206011 6.647004 4.180629e-11 0.3376341 0.6203335 1494Keeping/Excluding Covariates

If there are covariates that users would like to keep in the

balancing conditions regardless of whether they are selected in double

selection, we can use the X.keep argument to specify the

covariates to keep. On the other hand, if a priori we know some

combinations of the covariates are nonsensical, we can exclude them

explicitly by using the exclude argument. For example, we

can exclude any interaction that involves X1 and

X2:

out <- hbal(Treat = 'D', X = c('X1', 'X2', 'X3'), Y = 'Y', data = dat,

expand.degree = 3, exclude = list(c('X1', 'X2')))

summary(out) # X1.X2 and X1.X1.X2 removed from balancing scheme

#> Call:

#> hbal(data = dat, Treat = "D", X = c("X1", "X2", "X3"), Y = "Y",

#> expand.degree = 3, exclude = list(c("X1", "X2")))

#>

#> Treated Controls

#> 256 1244

#> Co/Tr Ratio = 4.86

#>

#> Groups

#> #Terms Penalty

#> linear 3 0

#> two-way 2 0

#> squared 2 0

#> squared*linear 2 0

#> cubic 2 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> X1 0.35 -0.11 0.35 0.46 0

#> X2 0.42 -0.07 0.42 0.49 0

#> X3 0.52 0.51 0.52 0.02 0

#> X1.X3 0.07 -0.02 0.07 0.12 0

#> X2.X3 0.21 -0.01 0.21 0.33 0

#> X1.X1 1.01 1.01 1.01 0.00 0

#> X2.X2 0.99 0.99 0.99 0.00 0

#> X1.X1.X3 0.55 0.52 0.55 0.03 0

#> X2.X2.X3 0.50 0.47 0.50 0.02 0

#> X1.X1.X1 0.93 -0.25 0.93 0.30 0

#> X2.X2.X2 1.16 -0.23 1.16 0.40 0

att(out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

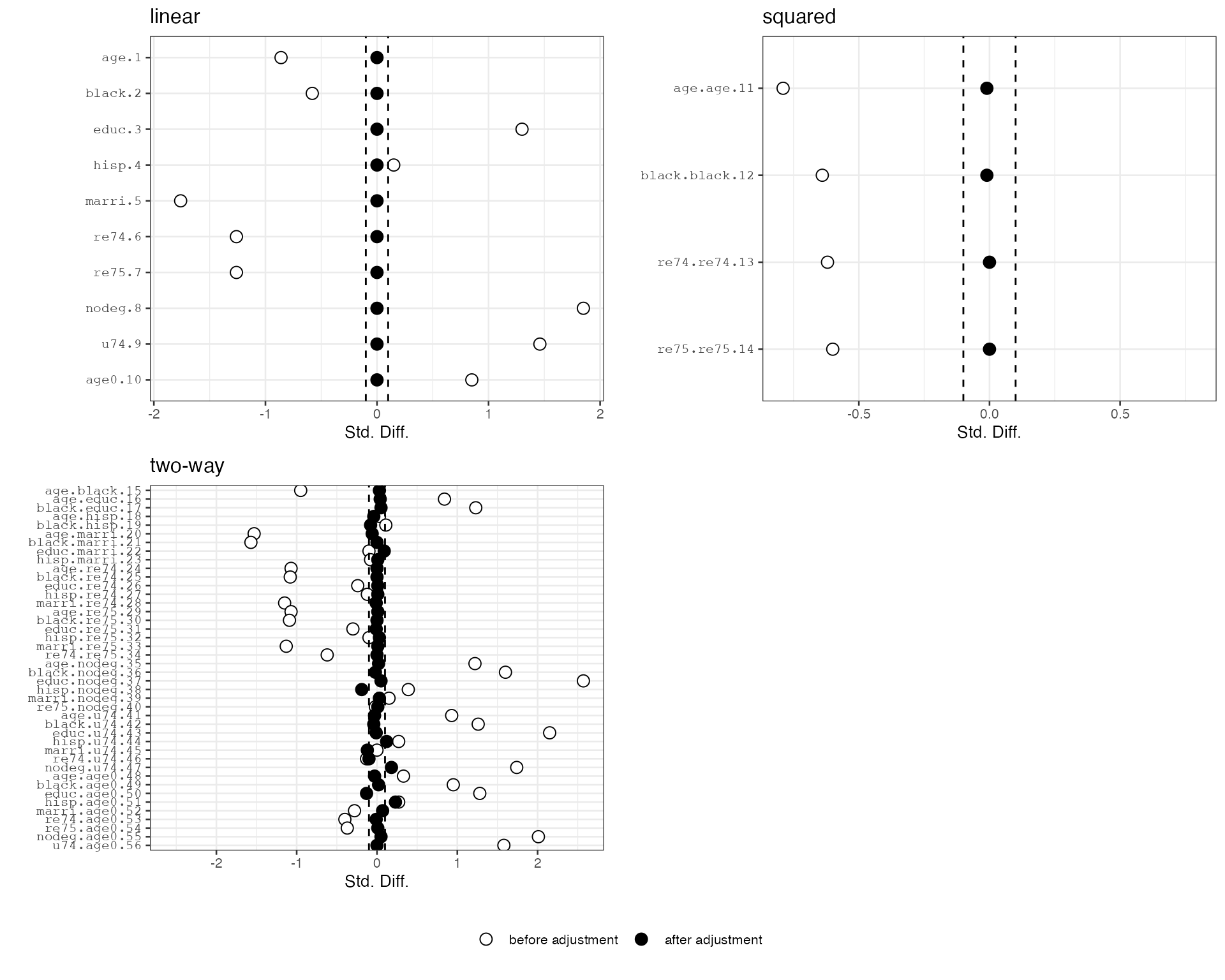

#> D 0.485784 0.07169999 6.775232 1.78421e-11 0.3451402 0.6264279 1487Example 1: Lalonde Data

To show the use of habl in practice, here we use habl on a dataset that contains the subset of the LaLonde (1986) dataset from Dehejia and Wahba (1999) and the Panel Study of Income Dynamics (PSID-1), which is also shipped with hbal.

data(hbal)

head(lalonde)

#> nsw age educ black hisp married re74 re75 re78 u74 u75 u78 nodegr

#> 1 0 47 12 0 0 0 0 0 0 1 1 1 0

#> 2 0 50 12 1 0 1 0 0 0 1 1 1 0

#> 3 0 44 12 0 0 0 0 0 0 1 1 1 0

#> 4 0 28 12 1 0 1 0 0 0 1 1 1 0

#> 5 0 54 12 0 0 1 0 0 0 1 1 1 0

#> 6 0 55 12 0 1 1 0 0 0 1 1 1 0First, we adjust for the linear terms only:

xvars <- c("age","black","educ","hisp","married","re74","re75","nodegr","u74","u75") # covariates

# hbal w/ level terms only

hbal.out <- hbal(Treat = 'nsw', X = xvars, Y = 're78', data = lalonde)

summary(hbal.out)

#> Call:

#> hbal(data = lalonde, Treat = "nsw", X = xvars, Y = "re78")

#>

#> Treated Controls

#> 185 2490

#> Co/Tr Ratio = 13.46

#>

#> Groups

#> #Terms Penalty

#> linear 10 0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> age 25.82 34.85 25.82 -0.86 0

#> black 10.35 12.12 10.35 -0.58 0

#> educ 0.84 0.25 0.84 1.30 0

#> hisp 0.06 0.03 0.06 0.15 0

#> marri 0.19 0.87 0.19 -1.76 0

#> re74 2095.57 19428.75 2100.16 -1.26 0

#> re75 1532.06 19063.34 1536.82 -1.26 0

#> nodeg 0.71 0.09 0.71 1.85 0

#> u74 0.60 0.10 0.60 1.46 0

#> age0 0.71 0.31 0.71 0.85 0

att(hbal.out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> nsw 2423.165 719.4805 3.367937 0.0007680966 1012.368 3833.962 2663Adding higher-order terms makes the treatment effect estimate closer

to the experimental benchmark (~$1800). As a result of cross-validation,

no penalty is imposed on the linear and squared terms. Note that

exclude=list(c("educ", "nodegr")) removes the nonsensical

interaction between educ and nodegr.

hbal.full.out <- hbal(Treat = 'nsw', X = xvars, Y = 're78', data = lalonde,

expand.degree = 2, cv = TRUE, exclude=list(c("educ", "nodegr")))

#> Crossvalidation...

summary(hbal.full.out)

#> Call:

#> hbal(data = lalonde, Treat = "nsw", X = xvars, Y = "re78", expand.degree = 2,

#> cv = TRUE, exclude = list(c("educ", "nodegr")))

#>

#> Treated Controls

#> 185 2490

#> Co/Tr Ratio = 13.46

#>

#> Groups

#> #Terms Penalty

#> linear 10 0

#> squared 4 0

#> two-way 42 100

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> age 25.82 34.85 25.82 -0.86 0.00

#> black 10.35 12.12 10.35 -0.58 0.00

#> educ 0.84 0.25 0.84 1.30 0.00

#> hisp 0.06 0.03 0.06 0.15 0.00

#> marri 0.19 0.87 0.19 -1.76 0.00

#> re74 2095.57 19428.75 2095.64 -1.26 0.00

#> re75 1532.06 19063.34 1532.08 -1.26 0.00

#> nodeg 0.71 0.09 0.71 1.85 0.00

#> u74 0.60 0.10 0.60 1.46 0.00

#> age0 0.71 0.31 0.71 0.85 0.00

#> age.age 717.39 1323.53 726.97 -0.79 -0.01

#> black.black 111.06 156.32 112.06 -0.64 -0.01

#> re74.re74 28141434.44 557148332.57 25567475.07 -0.62 0.00

#> re75.re75 12654752.23 548213776.79 12138371.63 -0.60 0.00

#> age.black 266.98 414.70 261.76 -0.95 0.03

#> age.educ 21.91 8.56 21.26 0.84 0.04

#> black.educ 8.70 2.60 8.43 1.23 0.05

#> age.hisp 1.36 1.16 1.63 0.03 -0.04

#> black.hisp 0.58 0.35 0.74 0.11 -0.08

#> age.marri 5.56 30.90 6.50 -1.53 -0.06

#> black.marri 1.96 10.47 1.94 -1.57 0.00

#> educ.marri 0.16 0.20 0.12 -0.10 0.09

#> hisp.marri 0.02 0.03 0.01 -0.08 0.01

#> age.re74 54074.04 704912.21 53890.91 -1.07 0.00

#> black.re74 22898.73 248073.37 22654.36 -1.08 0.00

#> educ.re74 1817.20 3646.09 1703.81 -0.24 0.01

#> hisp.re74 151.40 589.15 132.10 -0.12 0.01

#> marri.re74 760.63 17578.61 834.92 -1.15 -0.01

#> age.re75 41167.28 688282.61 38042.18 -1.07 0.01

#> black.re75 15880.57 244584.33 16095.74 -1.09 0.00

#> educ.re75 1257.04 3502.23 1316.30 -0.30 -0.01

#> hisp.re75 153.73 511.72 46.78 -0.10 0.03

#> marri.re75 654.34 17200.24 485.94 -1.13 0.01

#> re74.re75 13118590.79 523653961.37 11715080.77 -0.62 0.00

#> age.nodeg 18.78 3.50 18.54 1.22 0.02

#> black.nodeg 7.26 1.01 7.35 1.60 -0.02

#> educ.nodeg 0.60 0.01 0.59 2.57 0.05

#> hisp.nodeg 0.03 0.00 0.05 0.39 -0.19

#> marri.nodeg 0.11 0.07 0.11 0.15 0.03

#> re75.nodeg 307.44 372.31 286.15 -0.02 0.01

#> age.u74 15.98 3.99 16.38 0.93 -0.03

#> black.u74 6.15 1.15 6.31 1.26 -0.04

#> educ.u74 0.52 0.02 0.52 2.15 -0.01

#> hisp.u74 0.03 0.01 0.02 0.27 0.12

#> marri.u74 0.09 0.09 0.12 0.00 -0.12

#> re74.u74 43.85 483.27 361.33 -0.13 -0.10

#> nodeg.u74 0.59 0.07 0.53 1.74 0.18

#> age.age0 17.97 11.83 18.45 0.33 -0.03

#> black.age0 6.71 2.62 6.64 0.95 0.02

#> educ.age0 0.61 0.13 0.66 1.28 -0.13

#> hisp.age0 0.05 0.01 0.02 0.27 0.23

#> marri.age0 0.14 0.26 0.11 -0.28 0.07

#> re74.age0 1094.15 4511.11 1198.46 -0.40 -0.01

#> re75.age0 1134.96 4272.56 1013.44 -0.37 0.01

#> nodeg.age0 0.52 0.03 0.51 2.01 0.05

#> u74.age0 0.43 0.04 0.43 1.58 0.00

att(hbal.full.out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

#> nsw 2081.452 725.9504 2.867209 0.004174207 657.9566 3504.947 2617We can check the penalties applied to each group and the cavariate balance before and after balancing.

hbal.full.out$group.penalty

#> linear squared two-way

#> 0.000000e+00 7.997239e-03 1.000000e+02

plot(hbal.full.out)

Example 2: Black and Owens (2016)

The second example comes from Black and Owens

(2016), in which the authors study the effect of promotion

prospect to the Supreme Court on the behavior of circuit court judges.

Here we focus on whether circuit court judges who are on the shortlist

to fill Supreme Court vacancies (“contenders”) ruled in line with the

president as the outcome of interest. We load the dataset

contenderJudges, which is shipped with

hbal.

data(hbal)First, we take a look at the data structure. The outcome variable is

presIdeoVote and the treatment variable is

treatFinal0, indicating whether there was a Supreme Court

vacancy at the time. There are also 7 covariates on judge and court

characteristics and a variable judge that indicates the

judges’ names.

str(contenderJudges)

#> 'data.frame': 10171 obs. of 10 variables:

#> $ presIdeoVote: int 0 1 1 1 1 0 0 0 1 0 ...

#> $ treatFinal0 : int 1 1 1 1 1 1 1 1 1 1 ...

#> $ judgeJCS : num 0.28 0.581 0.199 0.406 -0.341 ...

#> $ presDist : num 0.0019 0.0552 0.3137 0.2302 0.9772 ...

#> $ panelDistJCS: num 0.0392 0.562 0.2485 0.4625 0.491 ...

#> $ circmed : num 0.0315 0.581 0.0375 0.013 0.047 ...

#> $ sctmed : num 0.227 0.122 -0.359 0.122 0.122 ...

#> $ coarevtc : int 0 0 0 1 1 1 0 1 0 1 ...

#> $ casepub : int 1 1 1 1 1 1 1 1 1 1 ...

#> $ judge : Factor w/ 68 levels "Alfred T. Goodwin",..: 34 31 9 4 3 59 67 52 16 34 ...We can estimate the effect of Supreme Court vacancy on judges’ rulings while controlling for functions of the covariates (to the second order). We see that contender judges are more likely to rule in line with the ideology of the sitting president during a Supreme Court vacancy.

xvars <- c("judgeJCS", "presDist", "panelDistJCS", "circmed", "sctmed", "coarevtc", "casepub")

out <- hbal(Treat = 'treatFinal0', X = xvars, Y = 'presIdeoVote', data = contenderJudges,

expand.degree = 2, cv = TRUE)

#> Crossvalidation...

summary(out)

#> Call:

#> hbal(data = contenderJudges, Treat = "treatFinal0", X = xvars,

#> Y = "presIdeoVote", expand.degree = 2, cv = TRUE)

#>

#> Treated Controls

#> 4490 5681

#> Co/Tr Ratio = 1.27

#>

#> Groups

#> #Terms Penalty

#> linear 7 0.0

#> squared 5 0.3

#> two-way 21 0.0

#>

#> Balance Table

#> Tr.Mean Co.Mean W.Co.Mean Std.Diff.(O) Std.Diff.(W)

#> judge 0.16 0.07 0.16 0.28 0.00

#> presD 0.17 0.45 0.17 -0.91 0.00

#> panel 0.34 0.29 0.34 0.23 0.00

#> circm 0.14 0.00 0.14 0.50 0.00

#> sctme 0.01 0.03 0.01 -0.07 0.00

#> coare 0.28 0.31 0.28 -0.07 0.00

#> casep 0.61 0.84 0.61 -0.53 0.00

#> judge.judge 0.13 0.12 0.14 0.10 -0.09

#> presD.presD 0.06 0.31 0.07 -0.84 -0.02

#> panel.panel 0.18 0.14 0.18 0.18 -0.03

#> circm.circm 0.08 0.08 0.09 0.01 -0.09

#> sctme.sctme 0.04 0.02 0.03 0.40 0.17

#> judge.presD 0.02 0.02 0.02 0.02 -0.03

#> judge.panel 0.05 0.03 0.05 0.15 0.00

#> presD.panel 0.04 0.13 0.05 -0.59 -0.02

#> judge.circm 0.05 0.05 0.05 0.02 -0.02

#> presD.circm 0.01 0.00 0.01 0.08 0.00

#> panel.circm 0.05 0.01 0.05 0.37 0.00

#> judge.sctme -0.02 0.01 -0.02 -0.54 -0.07

#> presD.sctme -0.01 0.02 -0.01 -0.41 0.00

#> panel.sctme 0.01 0.01 0.01 0.00 -0.03

#> circm.sctme 0.01 0.01 0.01 -0.08 -0.01

#> judge.coare 0.05 0.02 0.05 0.13 0.00

#> presD.coare 0.05 0.14 0.05 -0.39 0.00

#> panel.coare 0.10 0.09 0.10 0.04 -0.01

#> circm.coare 0.03 0.00 0.03 0.21 0.00

#> sctme.coare 0.01 0.01 0.01 -0.02 0.01

#> judge.casep 0.10 0.04 0.09 0.23 0.06

#> presD.casep 0.12 0.37 0.12 -0.83 -0.02

#> panel.casep 0.21 0.24 0.21 -0.09 0.03

#> circm.casep 0.05 -0.02 0.05 0.30 0.00

#> sctme.casep 0.00 0.01 0.00 -0.09 0.03

#> coare.casep 0.22 0.30 0.23 -0.16 -0.01

att(out)

#> Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper

#> treatFinal0 0.04317827 0.01256806 3.435556 0.0005937101 0.01854238 0.06781416

#> DF

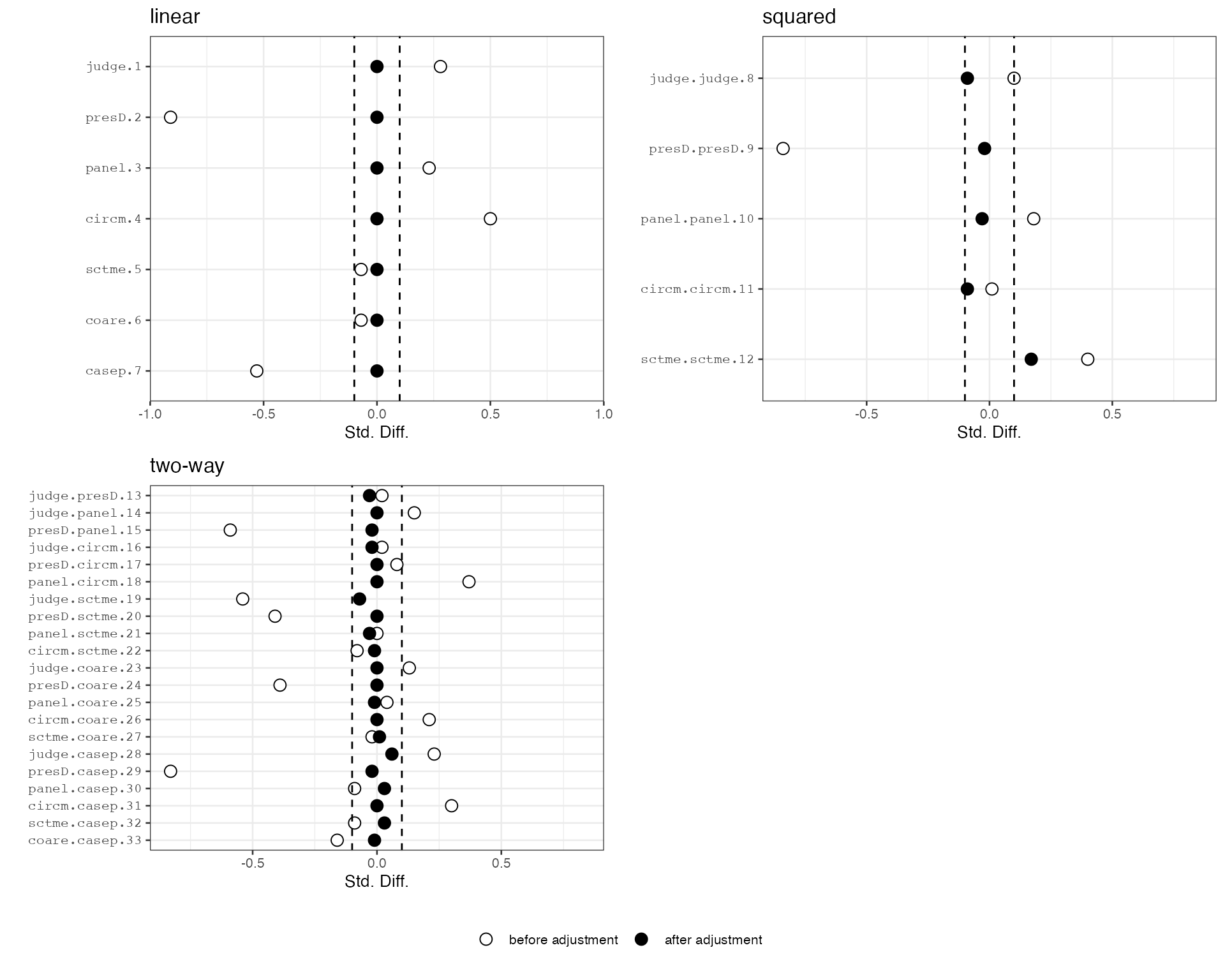

#> treatFinal0 10136We can further check covariate balance before and after balancing by checking the balance plots. Here we see that the linear terms are exactly balanced between the treatment and the control groups. Imbalance among higher-order terms and interactions are also significantly reduced.

plot(out)